Personal and Business Loans with Aadhaar Card: Government is Offering Loans up to ₹3 Lakh with 35% Subsidy

Access to affordable finance has always been a challenge for small entrepreneurs, self-employed individuals, and low-income families in India. To address this gap, the Government of India has introduced multiple Aadhaar-linked personal and business loan schemes that make borrowing simpler, faster, and more inclusive. Under selected government schemes, eligible beneficiaries can avail loans up to ₹3 lakh, and in some cases even higher, along with a subsidy of up to 35%, significantly reducing the repayment burden.

This article explains how Aadhaar-based loans work, which government schemes offer subsidies, eligibility criteria, application process, and the key benefits for individuals and small businesses.

What Are Aadhaar Card Loans?

An Aadhaar Card Loan is a loan facility where Aadhaar acts as the primary identity and KYC document. Instead of lengthy paperwork, Aadhaar enables quick verification, seamless digital processing, and easier access to credit—especially for people who may not have extensive financial records.

Aadhaar-linked loans are offered through:

- Government-backed schemes

- Public sector banks

- Regional Rural Banks (RRBs)

- Cooperative banks

- NBFCs partnered with government programs

These loans can be used for personal needs, micro and small businesses, self-employment, and income-generating activities.

Government Schemes Offering Loans up to ₹3 Lakh with Subsidy

Several flagship schemes support Aadhaar-based lending. The most relevant ones include:

1. Pradhan Mantri Mudra Yojana (PMMY)

PM Mudra Yojana is one of the most popular government loan schemes for micro and small enterprises.

Key Features:

- Loan amount: Up to ₹10 lakh

- Aadhaar card accepted as primary KYC

- No collateral required

- Categories: Shishu, Kishor, and Tarun

While Mudra loans do not directly provide a cash subsidy, they offer low interest rates and flexible repayment, making them ideal for small shop owners, vendors, service providers, and startups.

2. Prime Minister’s Employment Generation Programme (PMEGP)

PMEGP is the main scheme offering subsidies up to 35%, making it highly attractive for new entrepreneurs.

Key Features:

- Loan amount:

- Up to ₹25 lakh for manufacturing

- Up to ₹10 lakh for service sector

- Subsidy:

- Up to 35% for rural areas

- Up to 25% for urban areas

- Aadhaar card is mandatory

Example:

If you take a loan of ₹3 lakh under PMEGP and qualify for a 35% subsidy, ₹1.05 lakh is adjusted as subsidy, and you repay only the remaining amount.

3. Stand-Up India Scheme

This scheme promotes entrepreneurship among SC, ST, and women borrowers.

Key Features:

- Loan amount: ₹10 lakh to ₹1 crore

- Aadhaar-based KYC

- Composite loan for business and working capital

- No collateral in many cases (supported by CGTMSE)

Though subsidy is not always direct, the scheme offers favorable terms and government support.

Personal Loans Using Aadhaar Card

Apart from business loans, Aadhaar can also be used for small personal loans, especially through:

- Jan Dhan-linked accounts

- Government-supported financial inclusion programs

- Select NBFC and digital lending platforms

These loans are useful for:

- Medical expenses

- Education

- Emergency household needs

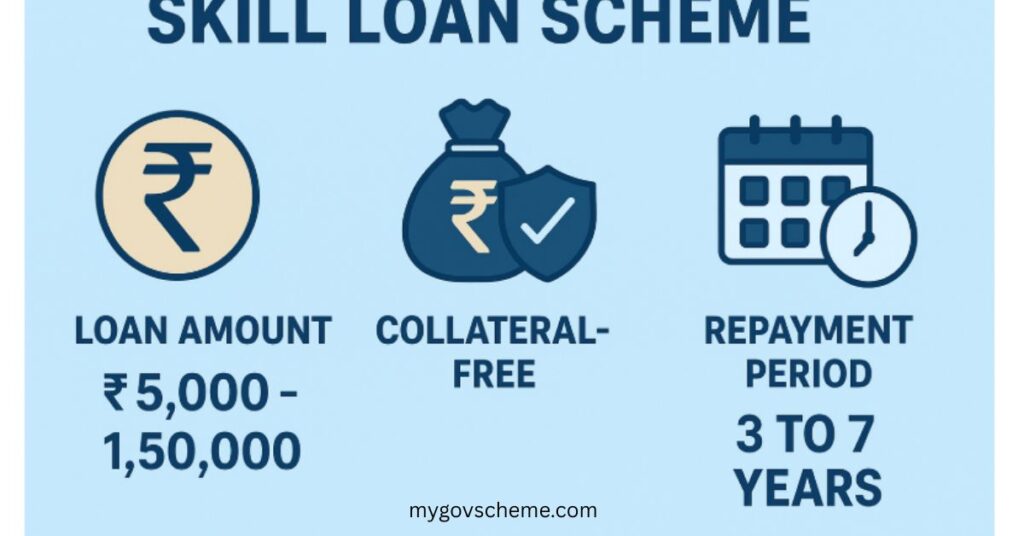

- Skill development

Personal loan amounts are usually smaller (₹10,000 to ₹2–3 lakh), but processing is fast due to Aadhaar-based e-KYC.

Eligibility Criteria (General)

While criteria vary by scheme, the common requirements include:

- Indian citizen

- Valid Aadhaar Card

- Age between 18 and 60 years

- Business plan (for business loans)

- No major loan default history

- Belonging to eligible category (for subsidy schemes)

For PMEGP and similar subsidy-based schemes, priority is given to:

- SC/ST candidates

- Women entrepreneurs

- OBC candidates

- Minority communities

- Rural applicants

Documents Required

Thanks to Aadhaar integration, documentation is minimal:

- Aadhaar Card

- PAN Card (in many cases)

- Bank account details

- Passport-size photographs

- Business proposal or project report (for business loans)

- Caste or category certificate (if applicable for subsidy)

How to Apply for Aadhaar-Based Government Loans

Step 1: Choose the right scheme (Mudra, PMEGP, Stand-Up India, etc.)

Step 2: Prepare a basic business plan (for business loans)

Step 3: Visit:

- Nearest bank branch, or

- Official government portals (like KVIC / bank websites)

Step 4: Submit Aadhaar-based application and documents

Step 5: Bank appraisal and verification

Step 6: Loan approval and subsidy adjustment (if applicable)

The subsidy amount is usually credited directly to the loan account, reducing the principal.

Benefits of Aadhaar-Based Loans with Subsidy

- Easy KYC & faster approval

- No or low collateral requirement

- Subsidy up to 35%, reducing repayment burden

- Encourages self-employment and entrepreneurship

- Ideal for first-time borrowers

- Promotes financial inclusion

Important Things to Remember

- Subsidy is not given in cash; it is adjusted against the loan

- Misuse of loan funds can lead to penalties

- Business loans require proper utilization and monitoring

- Timely repayment helps build credit score

Conclusion

The Government of India’s Aadhaar-linked personal and business loan schemes have opened new doors for millions of Indians. With loans up to ₹3 lakh and subsidies reaching 35%, these schemes make it easier than ever to start a small business, expand an existing one, or meet essential personal needs—without heavy paperwork or collateral.

If you have an Aadhaar card and a genuine requirement, exploring these government-backed loan options could be a smart financial move toward stability, self-reliance, and growth.